1. Context

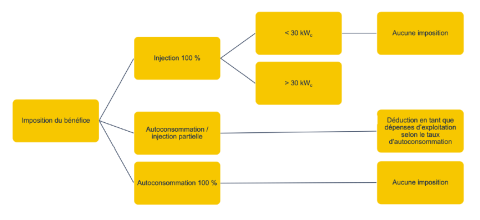

The tax treatment of the operation of a photovoltaic system differs according to the individual's choice, and one must distinguish between 3 cases:

- the operator sells the total production to the grid operator

- the operator consumes the generated electricity himself

- the operator consumes the amount of electricity needed for private or professional use, and only sells any surplus

In case 1, the operator of a photovoltaic system with an operated capacity above 30 kWp, sells the total electricity output produced to the grid operator. This is considered a business activity and the remuneration received from the sale of electricity constitutes taxable income.

In the case of a natural person who operates a small photovoltaic system (power: 1 kWp to 30 kWp) the Administration des Contributions Directes accepts, for the sake of simplification and as a matter of administrative tolerance, that the production of electricity is, generally speaking, a hobby that is not taken into account when determining taxable income.

In the case of self-consumption (case 2), the operation of the photovoltaic system is not considered a commercial activity and does not fall within one of the other categories of income listed in article 10 of the amended law on income tax (L.I.R.). There is therefore no taxable benefit but, depending on the use of the produced electricity, the expenses related to the photovoltaic system can be fully deductible as operating expenses. These different cases are described in Circular L.I.R. no. 14/2[1] and deal with the coverage of energy needs:

- of the taxpayer's household,

- of a commercial enterprise,

- a farm or forestry operation,

- the exercise of a liberal profession,

- of a combination of the above,

- of a tenant in the context of a building lease.

[1] Circular of the Directorate of Taxes L.I.R. no. 14/2 of 5 June 2023 replacing Circular L.I.R. no. 14/2 of 22 September 2021 with effect from the tax year 2023.

2. Definitions and terminology

Acquisition price

The acquisition price of the photovoltaic system must be considered separately, even where the solar installation is integrated into the building’s roof. The following are eligible: all items necessary for the photovoltaic installation, including, in particular, the invoice(s) for the installation issued by the supplier, the invoice for the installation of the meter issued by the network operator, etc.

State subsidies

The acquisition price is to be reduced by the amount of the state subsidy awarded by the Ministry of the Environment, Climate and Biodiversity

The subsidy is calculated using a formula based on the electrical power of the photovoltaic system. The maximum grant amount is €10,000, which is reached for a system with a capacity of 15 kWp.

If a battery is added, an additional subsidy may be awarded depending on its capacity. The maximum amount of this grant is €2,250, which is reached for a battery with a capacity of 9 kWh.

Condition: Self-consumption and waiving of a fixed feed-in tariff

Commercial profit

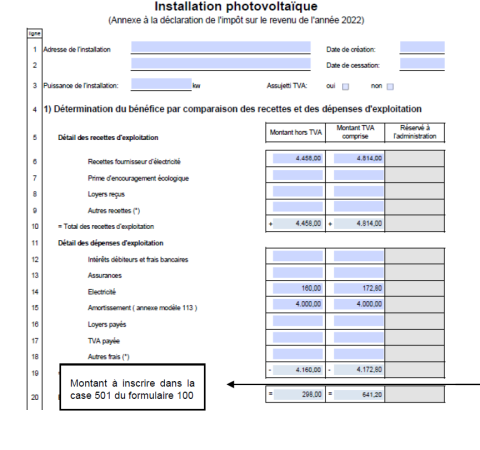

The commercial profit comprises the operating income and expenses of the photovoltaic installation. Income includes the sale of electricity generated (at the subsidised price) to the electricity network operator, relating directly to the year of the return, as shown in the interim payments and the final statement (where applicable). In the case of a first return, it may be that only the interim payments are available.

Operating expenses

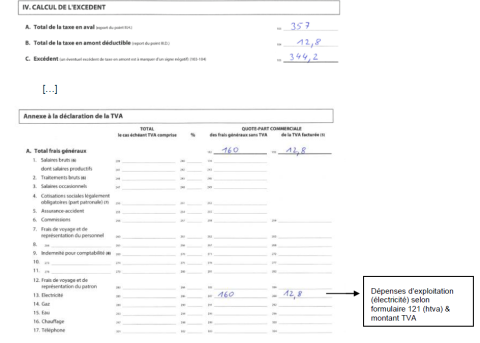

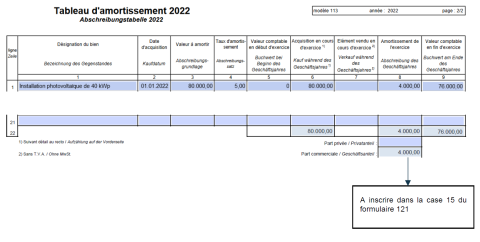

Expenses related to the photovoltaic installation, such as meter costs and interest on the financing of the installation, are fully deductible as operating expenses. Where the financing of the installation is covered by a general building loan, the interest is deductible in proportion to the cost of the installation relative to the total loan amount. The amount of depreciation also constitutes an operating expense deductible from the trading profit realised (see Form 121).

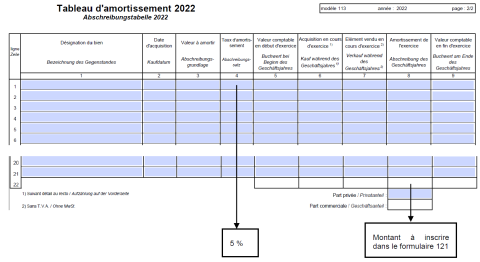

Amortisation

According to Circular L.I.R. No. 14/2 of 5 June 2023 (Directorate of Direct Taxation), the standard useful life of a photovoltaic installation is at least 20 years, and the applicable depreciation rate is set at 5% per year.

3. Forms

The tax return for a natural person operating a photovoltaic system consists of several forms, described below. The first declaration should be made for the year in which the investment was made, even if the taxpayer has not yet received any revenue. All supporting documents must be attached to the various forms (copies of invoices, copies of advances, etc.).

3.1. Income Tax Return (Form 100)

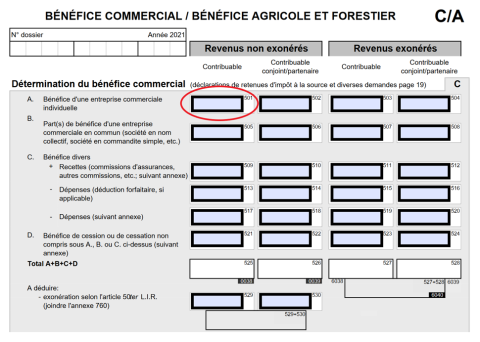

The realized business profit is entered in box 501 of the Income Tax Return (Déclaration pour l’impôt sur le revenu Form 100) under the heading "business profit" (page 5).

Sont à rajouter les annexes suivantes :

- Installation photovoltaïque (Formulaire 121)

- Acquisition d’immobilisations amortissables (Formulaire 113)

The following annexes must be added:

- Photovoltaic system (Form 121)

- Acquisitions of depreciable capital assets (Form 113)

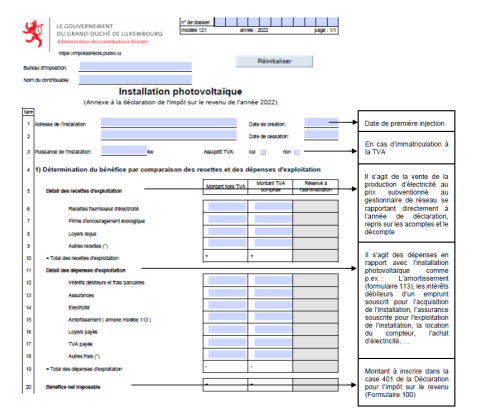

3.2. Photovoltaic system (Form 121)

This annex is used to determine the commercial benefit to entered in box 501 of the income tax return.

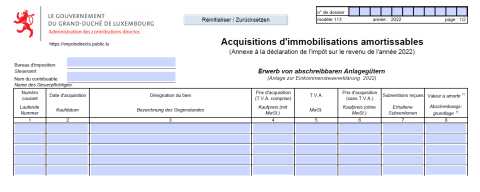

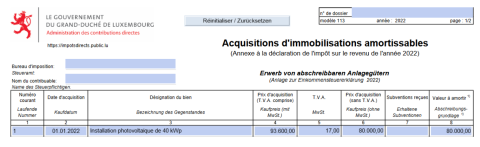

3.3. Acquisitions of depreciable capital assets (Form 113)

This annex is used to determine the depreciation to be deducted from the commercial benmercial. commercial.

4. Value Added Tax – VAT

Any individual who operates a photovoltaic system is considered to be liable for VAT. However, if the annual turnover is less than €50,000, the private individual is subject to the provisions of Article 57 of the VAT Act and benefits from the "régime particulier des petites entreprise” (special scheme for small businesses). In this case, they are exempt from making a VAT return, but must report their turnover for the previous year2 to the Registration Duties Authority by 1 March each year.

Anyone subject to the small business scheme is also free to opt for the standard VAT scheme. In this case, they get the right to reclaim input VAT and a regular VAT number.

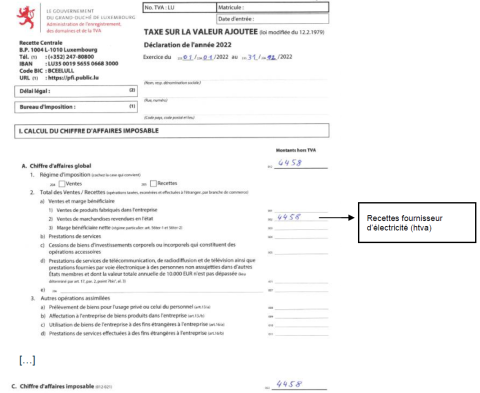

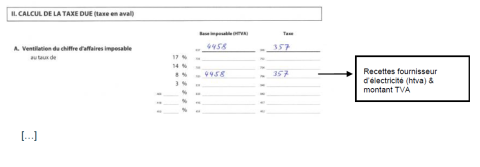

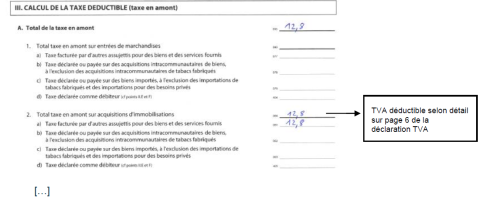

VAT registration entails the obligation to submit an annual VAT declaration (via MyGuichet or via forms to be downloaded from the AED website). In this case, the VAT on the investment (a priori 17 % in the case of a supplier from the Grand Duchy of Luxembourg) is deductible and the amount is taken into consideration when calculating the depreciation is the amount excluding VAT of the investment (reduced by the subsidies obtained). As for revenue, the VAT collected on the sale of electricity (8%) must be declared annually using the form that can be downloaded from the Administration de l'Enregistrement et des Domaines (http://www.aed.public.lu/formulaires/index.html).

More detailed information can be found in “article 1, paragraphe 2 du Règlement grand-ducal modifié du 21 janvier 1980” (article 1, paragraph 2 of the amended Grand-Ducal Regulation of 21 January 1980 laying down the conditions and procedures for the application of the tax exemption scheme provided for in respect of value added tax:

«L’assujetti soumis au régime de franchise de taxe prévu à l’article 57, paragraphe 1er, de la loi TVA est déchargé de l’obligation de dépôt de déclarations prévue à l’article 64, paragraphe 1er, de la loi TVA, à condition de ne pas avoir effectué, au cours de l’année civile, des prestations de services pour lesquelles le preneur du service non établi à l’intérieur du pays est le redevable de la taxe, et de n’être redevable, en vertu des dispositions de l’article 61, d’aucune taxe devenue exigible au cours de cette année civile.

L’assujetti visé à l’alinéa 1 doit cependant, avant le premier mars de l’année civile, informer l’Administration de l’enregistrement et des domaines, désignée ci-après par « l’administration », par écrit du montant de son chiffre d’affaires réalisé au cours de l’année civile précédente.

[1] Article 1, paragraphe 2, du Règlement grand-ducal modifié du 21 janvier 1980 ayant pour objet de fixer les conditions et modalités d'application du régime de franchise prévu en matière de taxe sur la valeur ajoutée (Article 1, paragraph 2, of the amended Grand-Ducal Regulation of 21 January 1980 laying down the conditions and procedures for the application of the exemption system provided for in respect of value added tax)

4.1 3% VAT

Since the 1st January 2023, the reduced rate of 3%3 has been applied to the supply and installation of solar panels, provided that the panels are installed on or in the immediate vicinity of private housing or public and other buildings serving the public interest. This reduced rate of 3% should not be confused with the 3% housing VAT.

All the components needed to install and operate the solar panels are covered by the reduced rate, including the following: photovoltaic panels (or hybrid solar collectors), mounting rails, DC and AC electrical wiring directly linked to the photovoltaic system, inverter, electrical protection devices, two-way meter; and for solar thermal panels: thermal solar collectors, mounting rails, DC and AC electrical wiring directly linked to the photovoltaic system, inverter, electrical protection devices, two-way meter; and for solar thermal panels: solar thermal collectors, mounting rails, DC and AC electrical wiring directly linked to the photovoltaic system, inverter, electrical protection devices, two-way meter; and for solar thermal panels: solar thermal collectors, mounting rails, DC and AC electrical wiring directly linked to the photovoltaic system: solar thermal collectors, mounting rails, insulated piping, solar storage tank, calorimeter, peripheral installations (power supply, regulation, heat exchangers); and of course the installation costs.

For photovoltaic solar panels, a storage installation (battery) is therefore not concerned.

In practical terms, this means :

- in the case of a completed supply/service, the applicable VAT rate is that in force on the day the supply/service is carried out (completed) (operative event)

- in the case of payments on account, the applicable VAT rate is that in effect on the day of collection of the payment on account.

5. Example of tax treatment for a 40 kWp installation

5.1. Assumptions

| Acquisition cost of a 40 kWp photovoltaic system on 01/01/2023 : | ||

| 80.000 € hVAT | 13.600 € (17 %) | |

| 93.600 € incl. VAT | ||

| Taxable person subject to VAT | ||

| Depreciation (5 %) : 4.000 € per year (5 % of 80.000 €) | ||

| Annual electricity production | 37.334 kWh/y | |

| Total feed-in with guaranteed feed-in tariff of €0.1194/kWh | Self-consumption with a negotiated tariff of 0,099[1] €/kWh | |

| Annual revenue | 4.458 € | 2.513[2] € |

[1]https://assets.ilr.lu/energie/Documents/ILRLU-1685561960-1173.pdf, 80 % de la moyenne de la période janvier-novembre 2023

[2] Taux d’autoconsommation de 15 %, donc injection de 31.734 kWh

5.2. Form 113 (depreciation)

5.3. Form 121 (Photovoltaic system)

5.4. Annual VAT return